TITLE 18. Public Revenues

Division 1. State Board of Equalization--Property Tax

Chapter 1. Valuation Principles and Procedures

Note • History

The rules in this subchapter govern assessors when assessing, county boards of equalization and assessment appeals boards when equalizing, and the State Board of Equalization, including all divisions of the property tax department.

NOTE

Authority cited: Section 15606, Government Code. Reference: Sections 110, 401, 1816, 1816.1, and Article 2, Chap. 3, Part 2, Div. 1, Revenue and Taxation Code.

HISTORY

1. New Subchapter 1 (Sections 1, 2, 3, 4 and 10) filed 6-23-67; effective thirtieth day thereafter (Register 67, No. 25).

2. Amendment of NOTE filed 10-26-77; effective thirtieth day thereafter (Register 77, No. 44).

3. Amendment filed 11-30-82; effective thirtieth day thereafter (Register 82, No. 49).

Note • History

(a) In addition to the meaning ascribed to them in the Revenue and Taxation Code, the words “full value”, “full cash value”, “cash value”, “actual value”, and “fair market value” mean the price at which a property, if exposed for sale in the open market with a reasonable time for the seller to find a purchaser, would transfer for cash or its equivalent under prevailing market conditions between parties who have knowledge of the uses to which the property may be put, both seeking to maximize their gains and neither being in a position to take advantage of the exigencies of the other.

When applied to real property, the words “full value”, “full cash value”, “cash value”, “actual value” and “fair market value” mean the price at which the unencumbered or unrestricted fee simple interest in the real property (subject to any legally enforceable governmental restrictions) would transfer for cash or its equivalent under the conditions set forth in the preceding sentence.

(b) When valuing real property (as described in paragraph (a)) as the result of a change in ownership (as defined in Revenue and Taxation Code, Section 60, et seq.) for consideration, it shall be rebuttably presumed that the consideration valued in money, whether paid in money or otherwise, is the full cash value of the property. The presumption shall shift the burden of proving value by a preponderance of the evidence to the party seeking to overcome the presumption. The presumption may be rebutted by evidence that the full cash value of the property is significantly more or less than the total cash equivalent of the consideration paid for the property. A significant deviation means a deviation of more than 5% of the total consideration.

(c) The presumption provided in this section shall not apply to:

(1) The transfer of any taxable possessory interest.

(2) The transfer of real property when the consideration is in whole, or in part, in the form of ownership interests in a legal entity (e.g., shares of stock) or the change in ownership occurs as the result of the acquisition of ownership interests in a legal entity.

(3) The transfer of real property when the information prescribed in the change in ownership statement is not timely provided.

(d) If a single transaction results in a change in ownership of more than one parcel of real property, the purchase price shall be allocated among those parcels and other assets, if any, transferred based on the relative fair market value of each.

NOTE

Authority cited: Section 15606, Government Code. Reference: Sections 110, 110.1, 401, Revenue and Taxation Code; Carlson v. Assessment Appeals Board No. 1 (1985) 167 Cal.App.3d 1004; Dennis v. County of Santa Clara (1989) 215 Cal.App.3d 1019.

HISTORY

1. Amendment filed 12-26-75; effective thirtieth day thereafter (Register 75, No. 52).

2. Amendment filed 8-21-85; effective thirtieth day thereafter (Register 85, No. 34).

3. Amendment filed 8-26-91; operative 9-25-91 (Register 91, No. 52).

4. Editorial correction of subsection (b) (Register 2002, No. 3).

In estimating value as defined in section 2, the assessor shall consider one or more of the following, as may be appropriate for the property being appraised:

(a) The price or prices at which the property and comparable properties have recently sold (the comparative sales approach).

(b) The prices at which fractional interests in the property or comparable properties have recently sold, and the extent to which such prices would have been increased had there been no prior claims on the assets (the stock and debt approach).

(c) The cost of replacing reproducible property with new property of similar utility, or of reproducing the property at its present site and at present price levels, less the extent to which the value has been reduced by depreciation, including both physical deterioration and obsolescence (the replacement or reproduction cost approach).

(d) If the income from the property is regulated by law and the regulatory agency uses historical cost or historical cost less depreciation as a rate base, the amount invested in the property or the amount invested less depreciation computed by the method employed by the regulatory agency (the historical cost approach).

(e) The amount that investors would be willing to pay for the right to receive the income that the property would be expected to yield, with the risks attendant upon its receipt (the income approach).

§4. The Comparative Sales Approach to Value.

Note • History

When reliable market data are available with respect to a given real property, the preferred method of valuation is by reference to sales prices. In using sales prices of the appraisal subject or of comparable properties to value a property, the assessor shall:

(a) Convert a noncash sale price to its cash equivalent by estimating the value in cash of any tangible or intangible property other than cash which the seller accepted in full or partial payment for the subject property and adding it to the cash portion of the sale price and by deducting from the nominal sale price any amount which the seller paid in lieu of interest to a lender who supplied the grantee with part or all of the purchase money.

(b) When appraising an unencumbered-fee interest, (1) convert the sale price of a property encumbered with a debt to which the property remained subject to its unencumbered-fee price equivalent by adding to the sale price of the seller's equity the price for which it is estimated that such debt could have been sold under value-indicative conditions at the time the sale price was negotiated and (2) convert the sale price of a property encumbered with a lease to which the property remained subject to its unencumbered-fee price equivalent by deducting from the sale price of the seller's equity the amount by which it is estimated that the lease enhanced that price or adding to the price of the seller's equity the amount by which it is estimated that the lease depressed that price.

(c) Convert a sale to the valuation date of the subject property by adjusting it for any change in price level of this type of property that has occurred between the time the sale price was negotiated and the valuation date of the subject property.

(d) Make such allowances as he deems appropriate for differences between a comparable property at the time of sale and the subject property on the valuation date, in physical attributes of the properties, location of the properties, legally enforceable restrictions on the properties' use, and the income and amenities which the properties are expected to produce. When the appraisal subject is land and the comparable property is land of smaller dimensions, and it is assumed that the subject property would be divided into comparable smaller parcels by a purchaser, the assessor shall allow for the cost of subdivision, for the area required for streets and alleys, for selling expenses, for normal profit, and for interest charges during the period over which it is anticipated that the smaller properties will be marketed.

NOTE

Authority cited: Section 15606, Government Code. Reference: Sections 110, 110.1, 110.5 and 401, Revenue and Taxation Code; and Article XIII A, Sections 1 and 2, California Constitution.

HISTORY

1. Amendment of subsections (c) and (d) filed 11-30-82; effective thirtieth day thereafter (Register 82, No. 49).

§6. The Reproduction and Replacement Cost Approaches to Value.

History

(a) The reproduction or replacement cost approach to value is used in conjunction with other value approaches and is preferred when neither reliable sales data (including sales of fractional interests) nor reliable income data are available and when the income from the property is not so regulated as to make such cost irrelevant. It is particularly appropriate for construction work in progress and for other property that has experienced relatively little physical deterioration, is not misplaced, is neither over- nor underimproved, and is not affected by other forms of depreciation or obsolescence.

(b) The reproduction cost of a reproducible property may be estimated either by (1) adjusting the property's original cost for price level changes and for abnormalities, if any, or (2) applying current prices to the property's labor and material components, with appropriate additions for entrepreneurial services, interest on borrowed or owner-supplied funds, and other costs typically incurred in bringing the property to a finished state (or to a lesser state if unfinished on the lien date). Estimates made under (2) above may be made by using square-foot, cubic-foot, or other unit costs; a summation of the in-place costs of all components; a quantity survey of all material, labor, and other cost elements; or a combination of these methods.

(c) The original cost of reproducible property shall be adjusted, in the aggregate or by groups, for price level changes since original construction by multiplying the cost incurred in a given year by an appropriate price index factor. When detailed investment records are unavailable for earlier years or when only a small percentage of the total investment is involved, the investments in such years may be lumped and factored to present price levels by means of an index number that represents the assessor's best judgment of the weighted average price change. If the property was not new when acquired by its present owner and its original cost is unknown, its acquisition cost may be substituted for original cost in the foregoing calculations.

(d) The replacement cost of a reproducible property may be estimated as indicated in (b) (2) of this section by applying current prices to the labor and material components of a substitute property capable of yielding the same services and amenities, with appropriate additions as specified in subsection (b) (2).

(e) Reproduction or replacement cost shall be reduced by the amount that such cost is estimated to exceed the current value of the reproducible property by reason of physical deterioration, misplacement, over- or underimprovement, and other forms of depreciation or obsolescence. The percentage that the remainder represents of the reproduction or replacement cost is the property's percent good.

(f) When the allowance made pursuant to paragraph (e) exceeds the amount included in the depreciation tables used by the assessor, the reasons therefor shall be noted in the appraisal record for the property and the amount thereof shall be ascertainable from the record.

HISTORY

1. New section filed 9-7-67; effective thirtieth day thereafter (Register 67, No. 36).

2. Amendment of subsection (f) filed 2-24-70; effective thirtieth day thereafter (Register 70, No. 9).

3. Amendment of subsections (b) and (d) filed 2-22-71; effective thirtieth day thereafter (Register 71, No. 9).

4. Repealer of subsection (f) and renumbering of subsections (g) and (h) to subsections (f) and (g) filed 2-18-77 as an emergency; effective upon filing (Register 77, No. 8).

5. Change without regulatory effect amending subsections (b) and (d) and repealing subsection (g) filed 12-19-97 pursuant to section 100, title 1, California Code of Regulations (Register 97, No. 51).

§8. The Income Approach to Value.

Note • History

(a) The income approach to value is used in conjunction with other approaches when the property under appraisal is typically purchased in anticipation of a money income and either has an established income stream or can be attributed a real or hypothetical income stream by comparison with other properties. It is the preferred approach for the appraisal of land when reliable sales data for comparable properties are not available. It is the preferred approach for the appraisal of improved real properties and personal properties when reliable sales data are not available and the cost approaches are unreliable because the reproducible property has suffered considerable physical depreciation, functional obsolescence or economic obsolescence, is a substantial over- or underimprovement, is misplaced, or is subject to legal restrictions on income that are unrelated to cost.

(b) Using the income approach, an appraiser values an income property by computing the present worth of a future income stream. This present worth depends upon the size, shape, and duration of the estimated stream and upon the capitalization rate at which future income is discounted to its present worth. Ideally, the income stream is divided into annual segments and the present worth of the total income stream is the algebraic sum (negative items subtracted from positive items) of the present worths of the several segments. In practical application, the stream is usually either

(1) divided into longer segments, such as the estimated economic life of the improvements and all time thereafter or the estimated economic life of the improvements and the year in which the improvements are scrapped and the land is sold, or

(2) divided horizontally by projecting a perpetual income for land and an income for the economic life of the improvements, or

(3) projected as a level perpetual flow.

(c) The amount to be capitalized is the net return which a reasonably well informed owner and reasonably well informed buyers may anticipate on the valuation date that the taxable property existing on that date will yield under prudent management and subject to such legally enforceable restrictions as such persons may foresee as of that date. Net return, in this context, is the difference between gross return and gross outgo. Gross return means any money or money's worth which the property will yield over and above vacancy and collection losses, including ordinary income, return of capital, and the total proceeds from sales of all or part of the property. Gross outgo means any outlay of money or money's worth, including current expenses and capital expenditures (or annual allowances therefor) required to develop and maintain the estimated income. Gross outgo does not include amortization, depreciation, or depletion charges, debt retirement, interest on funds invested in the property, or rents and royalties payable by the assessee for use of the property. Property taxes, corporation net income taxes, and corporation franchise taxes measured by net income are also excluded from gross outgo.

(d) In valuing property encumbered by a lease, the net income to be capitalized is the amount the property would yield were it not so encumbered, whether this amount exceeds or falls short of the contract rent and whether the lessor or the lessee has agreed to pay the property tax.

(e) Recently derived income and recently negotiated rents or royalties (plus any taxes paid on the property by the lessee) of the subject property and comparable properties should be used in estimating the future income if, in the opinion of the appraiser, they are reasonably indicative of the income the property will produce in its highest and best use under prudent management. Income derived from rental of properties is preferred to income derived from their operation since income derived from operation is the more likely to be influenced by managerial skills and may arise in part from nontaxable property or other sources. When income from operating a property is used, sufficient income shall be excluded to provide a return on working capital and other nontaxable operating assets and to compensate unpaid or underpaid management.

(f) When the appraised value is to be used to arrive at an assessed value, the capitalization rate is to include a property tax component, where applicable, equal to the estimated future tax rate for the area times the assessment ratio.

(g) The capitalization rate may be developed by either of two means:

(1) By comparing the net incomes that could reasonably have been anticipated from recently sold comparable properties with their sales prices, adjusted, if necessary, to cash equivalents (the market-derived rate). This method of deriving a capitalization rate is preferred when the required sales prices and incomes are available. When the comparable properties have similar capital gains prospects, the derived rate already includes a capital gain (or loss) allowance and the income to be capitalized should not include such a gain (or loss) at the terminus of the income estimate.

(2) By deriving a weighted average of the capitalization rates for debt and for equity capital appropriate to the California money markets (the band-of-investment method) and adding increments for expenses that are excluded from outgo because they are based on the value that is being sought or the income that is being capitalized. The appraiser shall weight the rates for debt and equity capital by the respective amounts of such capital he deems most likely to be employed by prospective purchasers.

(h) Income may be capitalized by the use of gross income, gross rent, or gross production multipliers derived by comparing sales prices of closely comparable properties (adjusted, if necessary, to cash equivalents) with their gross incomes, gross rents, or gross production.

(i) The provisions of this rule are not applicable to lands defined as open-space lands by Chapter 1711, Statutes of 1967, nor are they applicable in all respects to possessory interests.

NOTE

Authority cited: Section 15606, Government Code. Reference: Sections 110 and 401, Revenue and Taxation Code.

HISTORY

1. New section filed 12-19-67; effective thirtieth day thereafter (Register 67, No. 51).

2. Amendment of subsection (c) filed 12-22-76; effective thirtieth day thereafter (Register 76, No. 52).

3. Amendment of NOTE and subsection (c) filed 10-26-77; effective thirtieth day thereafter (Register 77, No. 44).

4. Amendment of subsections (c) and (f) filed 11-30-82; effective thirtieth day thereafter (Register 82, No. 49).

§10. Trade Level for Tangible Personal Property.

Note • History

(a) In appraising tangible personal property, the assessor shall give recognition to the trade level at which the property is situated and to the principle that property normally increases in value as it progresses through production and distribution channels. Such property normally attains its maximum value as it reaches the consumer level. Accordingly, tangible personal property shall be valued by procedures that are consistent with the general policies set forth herein.

(b) Except as provided by the following subdivisions, tangible personal property held by a consumer shall be valued at the amount of cash or its equivalent for which the property would transfer to a consumer of like property at the same trade level if exposed for sale on the open market. This value shall be estimated in accordance with regulations 4, 6, and 8. If a cost approach is employed, the cost shall include the full economic cost of placing the property in service. Full economic cost (i.e., replacement or reproduction cost), includes costs typically incurred in bringing the property to a finished state, including labor and materials, freight or shipping cost, installation costs, sales or use taxes, and additions for market supported entrepreneurial services (with appropriate allowances for trade, quantity, or cash discounts).-Full economic cost does not include extended service plans or extended warranties, supplies, or other assets or business services that may have been included in a purchase contract.

(c) Tangible personal property leased, rented, or loaned for a period of six months or less, having a tax situs at the place where the lessor normally keeps the property as provided in regulation 204, shall be valued at the amount of cash or its equivalent for which it would transfer to other lessors or retailers of like property. The value may be estimated by reference to the price at which the lessor could be expected to sell the property at fair market value to other lessors or retailers of like property. If that price is unknown, then the value may be estimated by reference to one or more of the following indicators of value: (1) the lessor's full economic cost of the property with a reasonable allowance for depreciation; (2) the cost indicated in subdivision (e) if the lessor is also the manufacturer; or (3) in accordance with subdivision (b).

(d) Tangible personal property leased, rented, or loaned for an extended but unspecified period or leased for a term of more than six months, having tax situs at the lessee's situs as provided in regulation 204, shall be valued by estimating the cash price or its equivalent for which the property could be sold at fair market value to an outside customer operating at the same level of trade as the lessee. If that price is unknown, then the value may be estimated by reference to one or more of the following indicators of value: (1) the lessee's full economic cost of the property with a reasonable allowance for depreciation; or (2) in accordance with subdivision (b).

(e) Tangible personal property acquired from internal sources for self-consumption or use, shall be valued by estimating the cash price or its equivalent for which the property could be sold at fair market value to an outside customer using the property at the same trade level, (with appropriate allowances for trade, quantity, or cash discounts). If that price is unknown, then the value may be estimated by reference to one or more of the following indicators of value: (1) the cost of property in its condition and location on the lien date, had it been acquired at fair market value from an outside supplier (including labor, materials, overhead, interdivisional and/or intercompany profits, interest on borrowed or owner supplied funds, sales or use tax, installation, and other costs incurred in bringing the property to a finished state, with appropriate allowances for trade, quantity, or cash discounts, and depreciation), or (2) in accordance with subdivision (b). The cost of the property in its condition and location on the lien date, had it been acquired at fair market value from an outside supplier, does not include extended service plans or extended warranties, supplies, other assets or business services. The quantity discount allowed a manufacturer, when it is its own largest customer, should be at least as large as that allowed its largest wholesale or retail customer.

(f) Tangible personal property in the hands of a person engaged in the function of a manufacturer, wholesaler, or retailer and a consumer shall be valued by estimating the cash price or its equivalent for which the property could be sold at fair market value to an outside customer operating at the same level of trade. The property shall be valued based on how it is situated or used on the lien date pursuant to subdivisions (b), (c), (d), and (e).

NOTE

Authority cited: Section 15606, Government Code. References: Sections 110 and 401, Revenue and Taxation Code.

HISTORY

1. Amendment filed 2-24-70 as an emergency; effective upon filing. Certificate of Compliance included (Register 70, No. 9).

2. Amendment filed 1-19-71; effective thirtieth day thereafter (Register 71, No. 4).

3. Amendment of subsection (f) filed 4-22-71; effective thirtieth day thereafter (Register 71, No. 17).

4. Amendment of section and Note filed 4-25-2000; operative 5-25-2000 (Register 2000, No. 17).

§20. Taxable Possessory Interests.

Note • History

(a) Possessory Interests. “Possessory interests” are interests in real property that exist as a result of:

(1) A possession of real property that is independent, durable, and exclusive of rights held by others in the real property, and that provides a private benefit to the possessor, except when coupled with ownership of a fee simple or life estate in the real property in the same person; or

(2) A right to the possession of real property, or a claim to a right to the possession of real property, that is independent, durable, and exclusive of rights held by others in the real property, and that provides a private benefit to the possessor, except when coupled with ownership of a fee simple or life estate in the real property in the same person; or

(3) Taxable improvements on tax-exempt land.

(b) Taxable Possessory Interests. “Taxable possessory interests” are possessory interests in publicly-owned real property. Excluded from the meaning of “taxable possessory interests”, however, are any possessory interests in real property located within an area to which the United States has exclusive jurisdiction concerning taxation. Such areas are commonly referred to as federal enclaves.

(c) Definitions. For purposes of this regulation:

(1) “Real property” is defined in section 104 of the Revenue and Taxation Code and includes public waters such as tidelands and navigable waters and waterways.

(2) “Possession” of real property means actual physical occupation. “Possession” requires more than incidental benefit from the public property, but requires actual physical occupation of the property pursuant to rights not granted to the general public; thus, the use of property such as hallways, common areas, and access roads at airports, stadiums, convention centers, or other public facilities by customers or employees of those who may lease other public property at the public facility of which they have exclusive use does not constitute “possession” of those hallways, common areas, or access roads by the lessee of the public property.

(3) A “right,” or a “claim to a right,” to the possession of real property means the right, or claim to a right, to actual physical occupation of real property. For purposes of this subdivision, a right, or a claim to a right, to the possession of real property may exist as a result of the possessor having or claiming to have: (i) a leasehold estate, an easement, a profit á prendre, or any other legal or equitable interest in real property of less than fee simple or life estate, regardless of how the interest may be identified in a deed, lease, or other document; or (ii) a use permit or agreement, such as a federal grazing permit, a permit to use a berth at a harbor, or a county use permit authorizing professional rafting outfitters to commercially operate on a river, that creates a legal or equitable interest in real property of less than fee simple or life estate.

(4) “Possessor” means the party or parties who hold the possessory interest, and any successors or assigns to such party or parties.

(5) “Independent” means a possession, or a right or claim to possession, if the possession or operation of the real property is sufficiently autonomous to constitute more than a mere agency. To be “sufficiently autonomous” to constitute more than a mere agency, the possessor must have the right and ability to exercise significant authority and control over the management or operation of the real property, separate and apart from the policies, statutes, ordinances, rules, and regulations of the public owner of the real property. For example, the control of an airport runway or taxiway by the Federal Aviation Administration (FAA) or another government agency or its agent is so complete that it precludes the airlines from exercising sufficient authority and control over the management or operation of the runways or taxiway and does not constitute sufficient “independence” to support a possessory interest.

(6) “Durable” means for a determinable period with a reasonable certainty that the possession of the real property by the possessor, or the possessor's right or claim with respect to the possession of the real property, will continue for that period.

(7) “Exclusive of rights held by others in the real property” means the enjoyment of an exclusive use of real property, or a right or claim to the enjoyment of an exclusive use together with the ability to exclude from possession by means of legal process others who may interfere with that enjoyment.

(A) For purposes of this subdivision, “exclusive uses” include the following types of uses of real property, as well as rights and claims to such types of uses of real property:

(1) The sole possession, occupancy, or use of real property,

(2) The possession, occupancy, or use of real property by co-tenants or co-owners as to leaseholds, easements, profits á prendre, or any other legal or equitable interests in real property of less than fee simple or life estate, where the uses constitute but a single use jointly enjoyed.

(3) The concurrent use of real property, not amounting to co-tenancy or co-ownership under subdivision (A)(2) above, by a person who has a primary or prevailing right to use the real property and/or to have its designees use the real property. For example, a public marina leases boat slips with a lease provision that allows the marina to rent a leased boat slip to a short-term user if the primary lessee is away; subject to the primary lessee's right to exclude the short-term user on the primary lessee's return. Under these facts, the primary lessee has a primary and prevailing right to use the leased boat slip. For purposes of this subdivision, concurrent use of real property demonstrating a primary or prevailing right also includes alternating uses of the same real property by more than one party, such as the case when certain premises are used by a professional basketball team on certain days of each week while a professional hockey team uses the same premises on certain other days.

(4) Concurrent uses of real property, not amounting to co-tenancy or co-ownership under subdivision (A)(2) above, by persons making qualitatively different uses of the real property. For purposes of this subdivision, qualitatively different uses of real property include: (i) those by persons making different kinds of uses of the same real property, such as the case when one person is developing mineral resources on real property while others are concurrently enjoying recreational uses on the same real property; and (ii) those where different persons have the right to concurrently enter onto and take different things from the same real property.

(5) Concurrent uses of real property, not amounting to co-tenancy or co-ownership under subdivision (A)(2) above, by persons engaged in qualitatively similar uses that diminish the quantity or quality of the real property. For purposes of this subdivision, uses that diminish the quantity and/or quality of the real property include: (i) grazing cattle; (ii) mining; (iii) the extraction of oil or gas; and (iv) the extraction of geothermal energy.

(6) Concurrent uses of real property, not amounting to co-tenancy or co-ownership under subdivision (A)(2) above, by persons engaged in qualitatively similar uses that do not diminish the quantity or quality of the real property, provided that the number of concurrent use grants is restricted. For purposes of this subdivision: “concurrent use grants” includes grants, permits, deeds, agreements, and other documents providing rights to the concurrent use of real property; and the number of concurrent use grants is “restricted” when the number of concurrent use grants is restricted either by law or pursuant to the policies or management decisions of the public owner of the real property or other public agency.

Example 1: Commercial rafting outfitters have a county use permit to commercially operate on a river. While any private recreational user may raft on the river without limitation or regulation, only approximately 80 commercial rafting outfitters are presently allowed to operate under permit on the river. The commercial rafting outfitters' use of the river is exclusive for purposes of this regulation since the number of commercial use permits issued by the county to commercial rafting outfitters is restricted, regardless of whether or not the commercial rafting outfitters' use of the river diminishes its quantity or quality.

Example 2: X operates a shuttle van service, picking up passengers at their homes and other locations, and transporting them to the airport. When the shuttle van reaches the airport, it utilizes the public street which surrounds the airport to drop passengers off at the various terminals at the airport. The street around the airport is available to all licensed drivers, for commercial and noncommercial uses. Neither the traffic laws, nor the policies or management decisions of the public owner of the airport facility restrict the number of users of the public street. In addition, under the assumed facts of this hypothetical, X's use of the public street surrounding the airport does not diminish the quantity or quality of the real property.

Given that (i) the shuttle vans using the public street are making qualitatively similar uses of that real property; (ii) there are no facts indicating that the quality or quantity of the real property is being diminished; and (iii) the number of users of the real property is not restricted, X's right to use the public street surrounding the airport is not exclusive, and X does not have a possessory interest in the public street surrounding the airport.

(B) A use of real property, or a right or claim to a use of real property, that does not contain one of the elements in subdivisions (A)(1) to (6) above, inclusive, shall be rebuttably presumed to be nonexclusive.

(C) In no event shall the presence of occasional trespassers or occasional interfering uses be sufficient in and of itself to make nonexclusive a use, or a right or claim to a use, that is otherwise exclusive for purposes of this regulation.

(8) “Private benefit” means that the possessor has the opportunity to make a profit, or to use or be provided an amenity, or to pursue a private purpose in conjunction with its use of the possessory interest. The use should be of some private or economic benefit to the possessor that is not shared by the general public. The fact that a possession of real property is not for a business or commercial purpose or that the possessor is a non-profit corporation does not preclude the possessor from being found to have received a “private benefit” from that possession.

NOTE

Authority cited: Section 15606(c), Government Code. Reference: Section 107, Revenue and Taxation Code.

HISTORY

1. New section filed 4-6-98; operative 5-6-98 (Register 98, No. 15).

§21. Taxable Possessory Interests-Valuation.

Note • History

(a) Definitions. For the purposes of this regulation:

(1) “Real property” is defined in rule 20(c)(1).

(2) “Possession” is defined in rule 20(c)(2).

(3) A “right” to the possession of real property includes a “claim to a right” to the possession of real property within the meaning of rule 20(c)(3).

(4) “Possessor” is defined in rule 20(c)(4).

(5) The “term of possession” of a taxable possessory interest means the term of possession for valuation purposes.

(6) The “stated term of possession” for a taxable possessory interest as of a specific date is the remaining period of possession as of that date as specified in the lease, agreement, deed, conveyance, permit, or other authorization or instrument that created, extended, or renewed the taxable possessory interest, including any option or options to renew or extend the specified period of possession if it is reasonable to assume that the option or options will be exercised.

(7) “Contract rent” means any compensation or payments, in cash or its equivalent, that are required to be paid or provided by a possessor under an authorization or instrument that creates a taxable possessory interest for the rights in real property provided by the taxable possessory interest.

(8) “Economic rent” means the estimated amount that would be paid by the possessor, on the valuation date in cash or its equivalent, for the rights in real property provided by the taxable possessory interest if (i) the rights to possession were offered in an open and competitive market and (ii) the public owner's interest in the property were not exempt or immune from taxation. Economic rent does not include payments by the possessor to the public owner that are not paid as consideration for rights in real property, such as payments for the rental of personal property, for the provision of security services, and for advertising and promotional services.

(9) “Creation” means the creation of a taxable possessory interest. Creation includes (i) an initial grant or other conveyance of a taxable possessory interest; (ii) a subsequent grant or other conveyance of additional land or improvements to a preexisting taxable possessory interest; or (iii) a subsequent grant or other conveyance of additional valuable property rights or uses to a preexisting taxable possessory interest.

(10) “Extension or renewal” means the lengthening of the period of possession of a taxable possessory interest, such as by the exercise of an option to extend or to renew a lease or permit.

(b) Rights to be Valued. Except as provided in subsection (f) or specifically provided otherwise by law, the rights to be valued in a taxable possessory interest are all rights in real property held by the possessor.

(1) The fair market value of a taxable possessory interest is not diminished by any obligation of the possessor to pay rent or to retire debt secured by the taxable possessory interest. In other words, the fair market value of a taxable possessory interest is the fair market value of the fee simple absolute interest reduced only by the value of the property rights, if any, granted by the public owner to other persons and by the value of the property rights retained by the public owner (excluding the public owner's right to receive rent).

(2) Examples of rights in real property that may be granted or retained by the public owner include the following: (i) the right to take possession of the property upon the termination of the taxable possessory interest due to the occurrence of an event such as the expiration of the contract term, a breach of agreement, or the happening of a condition that terminates the possessor's right to possession; (ii) the right to put the property to a higher and better use or otherwise restrict the possessor's use of the property; (iii) the right to terminate possession upon notice; (iv) the right to approve a sublessee or assignee; (v) the right to approve a loan secured by the taxable possessory interest; and (vi) the right to allow other possessors to use the property.

(c) Standard of Value. Assessors shall value a taxable possessory interest consistent with the requirements of subsections (a), (d), (e), and (f) of section 110 of the Revenue and Taxation Code. A taxable possessory interest subject to article XIII A of the California Constitution shall also be valued consistent with the requirements of section 110.1 of the Revenue and Taxation Code.

(d) Term of Possession for Valuation Purposes

(1) The term of possession for valuation purposes shall be the reasonably anticipated term of possession. The stated term of possession shall be deemed the reasonably anticipated term of possession unless it is demonstrated by clear and convincing evidence that the public owner and the private possessor have reached a mutual understanding or agreement, whether or not in writing, such that the reasonably anticipated term of possession is shorter or longer than the stated term of possession. If so demonstrated, the term of possession shall be the stated term of possession as modified by the terms of the mutual understanding or agreement.

(2) If there is no stated term of possession, the reasonably anticipated term of possession shall be demonstrated by the intent of the public owner and the private possessor, and by the intent of similarly situated parties, using criteria such as the following:

(A) The sale price of the subject taxable possessory interest and sales prices of comparable taxable possessory interests.

(B) The rules, policies, and customs of the public owner and of similarly situated public owners.

(C) The customs and practices of the private possessor and of similarly situated private possessors.

(D) The history of the relationship of the public owner and the private possessor and the histories of the relationships of similarly situated public owners and private possessors.

(E) The actions of the parties to the subject taxable possessory interest, including any amounts invested in improvements by the public owner or the private possessor.

(3) For the purposes of this regulation, a taxable possessory interest that runs from month to month, a taxable possessory interest without fixed term, or a taxable possessory interest of otherwise unspecified duration shall be deemed to be a taxable possessory interest with no stated term of possession.

(e) Valuation of Post-De Luz Taxable Possessory Interests. Except as specifically provided otherwise by law, and excluding a taxable possessory interest involving the production of gas, petroleum, or other hydrocarbons, the value of a taxable possessory interest created, extended, or renewed after December 24, 1955 (i.e., a “Post-De Luz” taxable possessory interest) may be estimated using one or more of the following methods, as appropriate for the taxable possessory interest being valued.

(1) Comparative Sales Approach to Value. In the comparative sales approach, a taxable possessory interest is valued using the sale price of the subject taxable possessory interest or sales prices of comparable taxable possessory interests, provided such interests shall have sold under the conditions of fair market value described in subsection (a) of section 110. A taxable possessory interest may be valued by the direct comparison method or the indirect comparison method.

(A) Direct Comparison Method

In the direct comparison method, the appraiser shall add the following to the sale price of the subject taxable possessory interest, or to the sale price of a comparable taxable possessory interest, to derive an indicator of the fair market value of the subject taxable possessory interest: (i) the present value on the sale date of any unpaid future contract rent for the term of possession; (ii) the fair market value on the sale date of any debt assumed by the buyer of the taxable possessory interest; and (iii) the present value on the sale date of any future costs that the buyer is contractually obligated to pay for the right of possession (e.g., the cost of site restoration at the end of the term of possession) less the present value on the sale date of any future benefits in addition to the right of possession or use that the buyer is contractually entitled to receive (e.g., the salvage value of, or reimbursement value for, improvements existing at the end of the term of possession). The unpaid future contract rent in (i) above shall be reduced by any expense necessary to maintain the income from the taxable possessory interest, including any element of “gross outgo” as defined in subsection (c) of rule 8.

When valuing a taxable possessory interest by comparison with the sales of other taxable possessory interests, the other taxable possessory interests shall be located sufficiently near the subject taxable possessory interest and shall be sufficiently alike in respect to character, size, situation, usability, zoning or other enforceable government restrictions on use (unless rebutted pursuant to subdivision (c) of section 402.1 of the Revenue and Taxation Code), and restrictions on possession or use contained in the legal authorization or instrument that created, extended or renewed the taxable possessory interest to make it clear that the comparable taxable possessory interests and the subject taxable possessory interest are comparable in value and that the cash equivalent price realized for the comparable taxable possessory interests may fairly be considered as shedding light on the value of the subject taxable possessory interest. The comparable sales also shall be sufficiently near in time to the valuation date of the subject taxable possessory interest. “Near in time to the valuation date'' does not include any sale more than 90 days after the valuation date.

(B) Indirect Comparison Method. In the indirect comparison method, a taxable possessory interest is valued by (i) estimating the fair market value on the valuation date of the possessor's rights in real property in the taxable possessory interest as if owned in perpetuity (i.e., the value of the fee simple absolute interest in such rights) using sales of fee simple absolute interests in properties that are comparable to the subject property as prescribed in section 402.5 of the Revenue and Taxation Code and whose highest and best use corresponds to, or is comparable with, the permitted use of the subject taxable possessory interest; and (ii) reducing this value by both the present value of those property rights for the period subsequent to the term of possession (i.e., the value of the fee simple absolute interest in such rights at the end of the term of possession) and the present value of all other rights of fee simple absolute ownership, if any, that are not provided to the possessor.

(2) Cost Approach to Value. In the cost approach, a taxable possessory interest is valued by (i) adding the estimated replacement cost new less depreciation of improvements that meet the requirements of the possessor's permitted use to the estimated value of the taxable possessory interest in land; and (ii) reducing this amount by the estimated present value of the improvements that shall revert to or be retained by the public owner at the end of the term of possession.

(A) The replacement cost new less depreciation of the improvements may be estimated as prescribed in subsections (d) and (e) of rule 6. The estimated value of the taxable possessory interest in land may be estimated using the comparative sales approach (direct or indirect method) or the income approach (direct or indirect method), as prescribed in subsections (e)(1) and (e)(3).

(B) If a possessor's property use is limited to specified time periods (e.g., certain hours of the day or certain days of the week) or is shared with other possessors, the value determined by the cost approach shall be reasonably allocated to each possessor in a manner that reflects each possessor's proportionate value of the right to possession.

(3) Income Approach to Value. In the income approach, a taxable possessory interest is valued by discounting the future net income that the interest in real property is capable of producing. A taxable possessory interest may be valued using the direct income method or the indirect income method.

(A) Direct Income Method. In the direct income method, a taxable possessory interest is valued by capitalizing the future net income that the taxable possessory interest is capable of producing under typical, prudent management for the term of possession.

(B) Indirect Income Method. In the indirect income method, a taxable possessory interest is valued by (i) estimating the fair market value of the possessor's rights on the valuation date as if owned in perpetuity (i.e., the value of the fee simple absolute interest in such rights) using the income approach to value as prescribed in rule 8; and (ii) reducing this value by the present value of the those rights for the period subsequent to the term of possession (i.e., the present value of the value of the fee simple interest in such rights at the end of the term of possession).

(C) Income to be Capitalized. The income to be capitalized in the valuation of a taxable possessory interest is the “net return” (as defined in subsection (c) of rule 8) attributable to the taxable possessory interest. The income to be capitalized may be based on either (i) the estimated economic rent for the subject taxable possessory interest or (ii) if the estimated economic rent is unreliable or unavailable, the estimated net operating income of a typical, prudent operator of the property subject to the taxable possessory interest. Rental income is preferable to operating income (i.e., income from operating a business) because operating income may be influenced by managerial skills and may derive, in part, from nontaxable property. The income to be capitalized must be attributable to the rights in real property in the subject taxable possessory interest and must reflect the restrictions on use inherent in the subject taxable possessory interest.

Economic rent

a. The economic rent of the subject taxable possessory interest may be estimated by reference to (i) the contract rent for the subject taxable possessory interest; (ii) contract rents for comparable taxable possessory interests; (iii) contract rents for comparable fee simple absolute interests in real property; or (iv) contract rents for other comparable interests in real property. All such contract rents shall have been negotiated in an open and competitive market involving real property reasonably comparable to the subject taxable possessory interest in terms of physical attributes, location, legally enforceable restrictions on the property's use, term of possession, and risk of cancellation of the taxable possessory interest by public owner. In addition, the contract rents shall have been negotiated sufficiently near in time to the valuation date as to shed light on the economic rent of the subject taxable possessory interest.

b. When using the contract rent of a taxable possessory interest as an indicator of the economic rent, the assessor shall add to the contract rent (i) an estimate of the amount, if any, by which the contract rent has been reduced because improvements have been constructed at the possessor's expense that will revert to the public owner at the end of the term of possession; and (ii) an estimate of the amount, if any, by which the contract rent has been reduced because the possessor will bear the cost of restoring the real property to its original condition on reversion to the public owner, including the cost of removing improvements (less any estimated salvage value of, or reimbursement value for, the improvements), or the cost of any similar obligation.

c. To arrive at the income to be capitalized, any expense necessary to maintain the income from the subject taxable possessory interest, including any element of “gross outgo” as defined in subsection (c) of rule 8, whether paid by the public owner or the possessor, must be deducted from the estimated economic rent if the expense will be paid out of the estimated economic rent.

Net Operating Income

a. Net operating income is gross operating income less allowed expenses. Gross operating income, allowed expenses, and net operating income are defined herein consistent with “gross return,” “gross outgo,” and “net return,” respectively, in subsection (c) of rule 8.

b. When valuing a taxable possessory interest using operating income, allowed expenses include the following: cost of goods sold (if applicable), typical operating expenses, typical management expense, an allowance for a return on working capital, and an allowance for a return on the value of any nontaxable property that contributes to the gross operating income. Typical operating expenses may include expenses for the rental of personal property, for the provision of security services, and for advertising and promotional services, provided such expenses are necessary for the production of the gross income. Typical operating expenses and typical management expense include expenses that an owner/operator typically would bear to maintain the property and to continue the production of income from the property but are borne by the public owner in the case of the subject taxable possessory interest.

c. Allowed expenses do not include the following: amortization, depreciation, depletion charges, debt retirement, interest on funds invested in the taxable possessory interest, the contract rent for the taxable possessory interest, property taxes on the taxable possessory interest, income taxes, or state franchise taxes measured by income.

(D) Capitalization Rate. Subsection (g) of rule 8 provides that a capitalization rate may be developed by either comparing the anticipated net incomes of recently sold comparable properties with their sales prices, or by deriving a weighted average of the capitalization rates (rates of return) for debt and equity capital appropriate to California money markets. In accordance with rule 8, the capitalization rate used in the valuation of a taxable possessory interest may be developed by (i) comparing the anticipated net incomes from comparable taxable possessory interests with their sales prices stated in cash or its equivalent and adjusted as described in subsection (e)(1)(A); (ii) comparing the anticipated net incomes of comparable fee simple absolute interests in real property with their sales prices stated in cash or its equivalent, provided the comparable fee properties are not expected to produce significantly higher net incomes subsequent to the subject taxable possessory interest's term of possession than during it; or (iii) by deriving a weighted average of the capitalization rates for debt and equity capital appropriate for the subject taxable possessory interest, weighting the separate rates of debt and equity by the relative amounts of debt and equity capital expected to be used by a typical purchaser of the subject taxable possessory interest. Consistent with subsection (f) of rule 8, the capitalization rate shall contain a component for property taxes where applicable

(f) Valuation of Pre-De Luz Taxable Possessory Interests. Except as specifically provided otherwise by law, and excluding a taxable possessory interest involving the production of gas, petroleum, or other hydrocarbons, the value of a taxable possessory interest created prior to December 24, 1955, and not since renewed or extended (i.e., a “Pre-De Luz” taxable possessory interest) is the excess of the fair market value on the valuation date of the taxable possessory interest over the present value of unpaid future contract rent for the unexpired term of possession (i.e., for the term of possession). This value may be estimated using one or more of the following methods, as appropriate for the taxable possessory interest being valued.

(1) Comparative Sales Approach to Value. A Pre-De Luz taxable possessory interest may be valued by the comparative sales approach using the direct comparison method or the indirect comparison method, as described in subsection (e)(1), but with the following modifications:

(A) Direct Comparison Method. In the direct comparison method, the present value of the unpaid future contract rent is not added to the sale price of the taxable possessory interest.

(B) Indirect Comparison Method. In the indirect comparison method, the value of the possessor's rights as if owned in fee is reduced by the present value of the unpaid future contract rent of the taxable possessory interest, as well as by the value of those property rights for the period subsequent to the term of possession.

(2) Cost Approach to Value. A Pre-De Luz taxable possessory interest may be valued by the cost approach as described in subsection (e)(2), but the present value of any unpaid future contract rent of the taxable possessory interest in land for the term of possession is also deducted.

(3) Income Approach to Value. A Pre-De Luz taxable possessory interest may be valued by the income approach using the direct income method or the indirect income method, as described in subsection (e)(3), but with the following modifications:

(A) Direct Income Method. In the direct income method, the net income to be capitalized is reduced by the unpaid future contract rent for the term of possession, as well as by allowed expenses.

(B) Indirect Income Method. In the indirect income method, the present value of the unpaid future contract rent for the term of possession is deducted from the value of the fee interest, as well as the deduction of the present value of the property rights for the period subsequent to the term of possession.

NOTE

Authority cited: Section 15606, Government Code. References: Sections 107 and 107.1, Revenue and Taxation Code.

HISTORY

1. New section filed 1-19-71; effective thirtieth day thereafter (Register 71, No. 4).

2. Amendment of subsection (b) filed 12-26-75; effective thirtieth day thereafter (Register 75, No. 52).

3. Amendment of NOTE filed 10-26-77; effective thirtieth day thereafter (Register 77, No. 44).

4. Amendment of first paragraph, repealer of subsections (a)-(e)(6), subsection relettering, and amendment of Note filed 4-6-98; operative 5-6-98 (Register 98, No. 15).

5. Amendment of section heading and repealer and new section filed 6-11-2002; operative 7-11-2002 (Register 2002, No. 24).

6. Change without regulatory effect amending subsection (e)(1)(A) filed 1-14-2003 pursuant to section 100, title 1, California Code of Regulations (Register 2003, No. 3).

§22. Continuity of Possessory Interests.

Note • History

(a) The continuity of possession or exclusive use necessary to establish a possessory interest will vary according to the location and character of the property. The continuity of use necessary for finding a possessory interest to exist is satisfied when the possessor of the property uses it to substantially the same extent as would an owner engaged in the same activity.

(b) Standards for determining the existence of taxable possessory interests based on continuity are:

(1) Actual or constructive possession or exclusive use of property on the lien date for the current year.

(2) Recurrent possession or exclusive use, whether or not the period extends through the lien date, when there is a history on the lien date of recurring use by the present or former possessors making a similar use of the property.

(3) Infrequent actual possession or exclusive use on a recurrent basis when the continuation of the right to possession or exclusive use is conditioned on or evidenced by the possessor having made a contribution to the value of the property by way of investment on or near the property occupied.

NOTE

Authority cited: Section 15606, Government Code. Reference: Sections 107, 107.1 and 107.4, Revenue and Taxation Code.

HISTORY

1. New section filed 1-19-71; effective thirtieth day thereafter (Register 71, No. 4).

2. Amendment of NOTE filed 10-26-77; effective thirtieth day thereafter (Register 77, No. 44).

§23. Written Agreements As to Term of Possessory Interests. [Repealed]

Note • History

NOTE

Authority cited: Section 15606, Government Code. Reference: Sections 107, 107.1 and 107.4, Revenue and Taxation Code.

HISTORY

1. New section filed 1-19-71; effective thirtieth day thereafter (Register 71, No. 4).

2. Amendment to NOTE filed 10-26-77; effective thirtieth day thereafter (Register 77, No. 44).

3. Repealer filed 6-11-2002; operative 7-11-2002 (Register 2002, No. 24).

§24. Possessory Interest Rights to Be Valued. [Repealed]

Note • History

NOTE

Authority cited: Section 15606, Government Code. Reference: Sections 107, 107.1 and 107.4, Revenue and Taxation Code.

HISTORY

1. New section filed 1-19-71; effective thirtieth day thereafter (Register 70, No. 4).

2. Amendment to NOTE filed 10-26-77; effective thirtieth day thereafter (Register 77, No. 44).

3. Repealer filed 6-11-2002; operative 7-11-2002 (Register 2002, No. 24).

§25. Valuation of Post-deLuz Possessory Interests. [Repealed]

Note • History

NOTE

Authority cited: Section 15606, Government Code. Reference: Sections 107, 107.1 and 107.4, Revenue and Taxation Code.

HISTORY

1. New section filed 1-19-71; effective thirtieth day thereafter (Register 71, No. 4).

2. Amendment of NOTE filed 10-26-77 effective thirtieth day thereafter (Register 77, No. 44).

3. Repealer filed 6-11-2002; operative 7-11-2002 (Register 2002, No. 24).

§26. Valuation of Pre-deLuz Possessory Interests. [Repealed]

Note • History

NOTE

Authority cited: Section 15606, Government Code. Reference: Section 107.1, Revenue and Taxation Code.

HISTORY

1. New section filed 1-19-71; effective thirtieth day thereafter (Register 71, No. 4).

2. Repealer filed 6-11-2002; operative 7-11-2002 (Register 2002, No. 24).

§27. Valuation of Possessory Interests for the Production of Hydrocarbons.

Note • History

(a) The taxable value of all possessory interests for the production of gas, petroleum, and other hydrocarbon substances from beneath the surface of the earth shall be determined by application of the comparative sales or income approach in the manner prescribed in subsections (e)(1) or (e)(3) of Regulation 21, except as provided in subsection (b) of this regulation.

(b) The taxable value of a possessory interest for the production of hydrocarbon substances from beneath the surface of the earth shall be determined by application of the comparative sales or income approach in the manner prescribed in subsections (f)(1) or (f)(3) of Regulation 21 if:

(1) the interest was created or last extended or renewed on or before July 26, 1963, and the rate of royalties or other right to share in production was not reduced because of an increase in the assessed value of such interest; or

(2) the interest was created on or before July 26, 1963, and has been extended or renewed thereafter pursuant to authority which prohibits reduction of the rate of royalty or other right to share in production because of an increase in the assessed value of such interest.

NOTE

Authority cited: Section 15606, Government Code. Reference: Sections 107, 107.2 and 107.3, Revenue and Taxation Code.

HISTORY

1. New section filed 1-19-71; effective thirtieth day thereafter (Register 71, No. 4).

2. Editorial correction deleting footnote filed 7-30-82 (Register 82, No. 31).

3. Change without regulatory effect amending section and Note filed 3-18-2005 pursuant to section 100, title 1, California Code of Regulations (Register 2005, No. 11).

§28. Examples of Taxable Possessory Interests.

Note • History

The following are examples of commonly encountered taxable possessory interests:

(a) The right to explore for, capture, and reduce to possession gas, petroleum, and other hydrocarbons in public lands.

(b) The possession of an employee in housing owned by a public agency, irrespective of whether occupancy of the housing is a condition of employment except when the facility also serves as the employee's work area to which the employer has full access.

(c) The right to cut and remove standing timber on public lands.

(d) The right to graze livestock or raise forage on public lands.

(e) The possession of public property at harbors, factories, airports, golf courses, marinas, recreation areas, parks, and stadiums. Possessory interests may include land subject to the ultimate grant of a United States patent, commercial and industrial sites, and water rights.

NOTE

Authority cited: Section 15606, Government Code. Reference: Sections 107, 107.1, 107.2, 107.3 and 107.4, Revenue and Taxation Code.

HISTORY

1. New section filed 1-19-71; effective thirtieth day thereafter (Register 71, No. 4).

2. Amendment of NOTE filed 10-26-77; effective thirtieth day thereafter (Register 77, No. 44).

§29. Possessory Interests in Taxable Government-Owned Real Property.

Note • History

(a) Definitions. For purposes of this rule:

(1) “Assessed value” is defined in subdivision (a) of section 135 of the Revenue and Taxation Code.

(2) “Improvements” are defined in rule 122.

(3) “Land” is defined in rule 121.

(4) A “lease for agricultural purposes” is a lease for the purpose of the production or husbandry of plants or animals, including gardening, horticulture, fruit growing, and the storage and marketing of agricultural products.

(5) “Other taxable improvements” are improvements owned by a local government outside of its boundaries that are taxable for property tax purposes pursuant to section 11(a), excluding taxable replacement improvements.

(6) “Real property” is the appraisal unit of real property, as defined in section 104 of the Revenue and Taxation Code, that persons in the marketplace commonly buy and sell as a unit or that is normally valued separately.

(7) “Section 11” means section 11 of Article XIII of the California Constitution.

(8) The “section 11 taxable possessory interest limitation amount” means the fair market value of the taxable government-owned real property on the lien date less the section 11 value of the taxable government-owned real property on the lien date.

(9) The “section 11 value of taxable government-owned real property” means the sum of: (i) the section 11 assessment amount for the taxable lands included in the real property on the lien date, computed pursuant to subdivisions (b) and (c) of section 11; (ii) the section 11 assessment amount for any taxable replacement improvements included in the real property on the lien date computed pursuant to the provisions of subdivision (d) of section 11; and (iii) the fair market value of other taxable improvements included in the real property on the lien date, if any.

(10) “Taxable government-owned real property” is real property owned by a local government outside of its boundaries that is taxable for property tax purposes pursuant to section 11(a).

(11) “Taxable lands” are lands owned by a local government outside of its boundaries that are taxable for property tax purposes pursuant to section 11(a).

(12) “Taxable possessory interest” is defined in rule 20.

(13) “Taxable replacement improvements” are improvements owned by a local government outside of its boundaries that are taxable for property tax purposes pursuant to section 11(a) because they were constructed by the local government to replace improvements that were taxable when acquired.

(14) The “total assessed value of all taxable possessory interests” means the aggregate assessed values of all taxable possessory interests in an appraisal unit of taxable government-owned real property on the lien date.

(b) Taxable possessory interests in taxable government-owned real property.

Except as set forth below in subsection (c) of this regulation, taxable possessory interests in taxable government-owned real property, excluding those created as a result of the possessor having a lease for agricultural purposes, shall be assessed and taxed for purposes of property taxation in the same manner as other taxable possessory interests.

(c) Limitation on the assessment of taxable possessory interests in taxable government-owned real property.

On each lien date, the total assessed value of all taxable possessory interests in an appraisal unit of taxable government-owned real property shall be determined. If the total assessed value of all taxable possessory interests on the lien date exceeds the section 11 taxable possessory interest limitation amount on the lien date, then the assessed values of the taxable possessory interests shall be reduced as follows: (i) if there is only one taxable possessory interest in the appraisal unit of taxable government-owned real property on the lien date, then the assessed value of that taxable possessory interest shall be reduced so that it does not exceed the section 11 taxable possessory interest limitation amount; or (ii) if there is more than one taxable possessory interest in the appraisal unit of taxable government-owned real property on the lien date, then the assessed value of each such taxable possessory interest shall be ratably reduced in the proportion that it bears to the total assessed value of all taxable possessory interests until the total assessed value of all taxable possessory interests no longer exceeds the section 11 taxable possessory interest limitation amount.

NOTE

Authority cited: Section 15606(c), Government Code. Reference: Article XIII, Section 11, California Constitution.

HISTORY

1. New section filed 1-10-2002; operative 2-9-2002 (Register 2002, No. 2).

§31. Petroleum Products Value Schedule. [Repealed]

Note • History

NOTE

Authority cited: Sec. 15606, Gov. Code. Reference: Articles 1 and 1.5, Chapter 1, Part 3, Division 1 and Sections 110, 401 and 401.5, Revenue and Taxation Code.

HISTORY

1. New section filed 12-14-67; effective thirtieth day thereafter (Register 67, No. 50).

2. Amendment of NOTE filed 10-26-77; effective thirtieth day thereafter (Register 77, No. 44).

3. Repealer filed 9-22-80; effective thirtieth day thereafter (Register 80, No. 39).

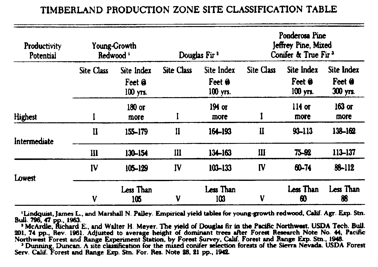

§41. Market Value of Timberland.

Note • History

(a) The Timber Appraisal Unit. In determining the timber to be valued as a unit, there shall be combined those parcels having:

(1) The same legal ownership. Timber sale contracts shall not be included in the unit.

(2) Commercial timber production as a dominant use.

(3) Geographical and physical conditions which permit similar treatment and economic removal of the timber to a common processing center. The typical practices of timberland owners and timber purchasers shall be used as a guide to indicate the geographical areas which are suitable for inclusion in the unit. Parcels shall not be excluded from the unit because they are outside the county, or because they are eligible for assessment under section 423.5 of the Revenue and Taxation Code.

(b) Immediate Harvest Value of Timber. The immediate harvest value of the timber on each of the separate parcels in the unit shall be determined. Immediate harvest value is the amount of cash or its equivalent for which timber would be transferred from a willing and informed seller to a willing and informed buyer, both seeking to maximize their incomes, if the timber could be harvested in the forthcoming year. The appraiser must consider all elements of value, such as volume by species, quality, defect, market conditions, volume per acre, size of timber, accessibility, topography, logging conditions, and distance from a processing center capable of utilizing the timber.

(c) Market Value of Timber. This section shall only apply to timber in the unit not eligible for assessment under section 423.5 of the Revenue and Taxation Code. The immediate harvest value of the timber on the timber appraisal unit is synonymous with market value if all the merchantable timber may reasonably be harvested in the forthcoming year. If the immediate harvest value of the timber on the appraisal unit is not synonymous with market value, it shall be converted to market value by application of a valuation factor to the immediate harvest value of the timber on each parcel in the unit. In determining the valuation factor, the appraiser shall consider the effect on market value of the total timber volume on the unit and the length of time over which the owner and knowledgeable prospective purchasers might reasonably be expected to harvest the timber, as indicated by sales of comparable timbered properties.

(d) Market Value of Timberland. This section shall only apply to areas in the unit not eligible for assessment under section 423.5 of the Revenue and Taxation Code. The market value of the timber on each parcel in the appraisal unit shall be added to the market value of the land as determined by the comparative sales approach. When land included within the timber appraisal unit has uses in addition to timber production, the appraiser shall determine its value with consideration for such uses, as evidenced by recent sales of comparable land. Allowances must be made for the value of any trees or improvements included in the sales of properties used as indicators of the value of land in the appraisal unit.

NOTE

Authority cited: Section 15606, Government Code. Reference: Sections 110, 401, 423.5, 1816.1 and 1816.2, Revenue and Taxation Code.

HISTORY

1. New section filed 3-29-68; effective thirtieth day thereafter (Register 68, No. 13).

2. Correctory amendment filed 5-17-68; effective upon filing (Register 68, No. 19).

3. Amendment filed 12-22-72; effective thirtieth day thereafter (Register 72, No. 52).

4. Amendment of NOTE filed 10-26-77; effective thirtieth day thereafter (Register 77, No. 44).

5. Editorial correction of NOTE filed 3-15-83 (Register 83, No. 12).

§45. Separate Determination of Value for Owner-Occupied Residential Dwellings. [Repealed]

Note • History

NOTE

Authority cited: Section 15606, Government Code. Reference: Section 401.6, Revenue and Taxation Code.

HISTORY

1. New section filed 4-21-78 as an emergency; effective upon filing (Register 78, No. 16).

2. Correction of adoption date filed 5-12-78 (Register 78, No. 16).

3. Certificate of Noncompliance (Repealer by operation of Section 11422.1, Gov. C.) filed 7-19-78 (Register 78, No. 29).

§51. Agreements Qualifying Land for Assessment As Open-Space Lands.

Note • History

An agreement made pursuant to the Land Conservation Act of 1965 prior to November 10, 1969, qualifies for restricted-use assessment pursuant to sections 423 and 426 of the Revenue and Taxation Code if, taken as a whole, it provides restrictions, terms, and conditions which are substantially similar to or more restrictive than those which were required by such act for a contract at the time the agreement became effective or which have subsequently been made less restrictive by the Legislature.

(a) Mandatory Provisions. The agreement must contain provisions at least as restrictive as the following:

(1) An initial term of years sufficient to make the agreement effective for ten successive lien dates and an annual renewal date at which time another year is automatically added to the term unless a notice of nonrenewal is given prior to such date.

(2) An exclusion of uses for the duration of the agreement other than agricultural uses and compatible uses as defined by the Land Conservation Act, the agreement, or the resolution establishing the agricultural preserve in which the property is located.

(3) A provision making the agreement binding upon and inuring to the benefit of all successors in interest of the owner.

(b) Disqualifying Provisions. An agreement in order to qualify for restricted use assessment must not contain any of the following:

(1) A provision purporting to bind the assessor to a particular assessment formula.

(2) A provision nullifying the agreement by reason of the owner's death or factors arising because of his death.

(c) Cancellation. The agreement may contain a cancellation provision as to all or part of the land if the following procedures are required under the terms of the agreement:

(1) Cancellation by mutual agreement, which may consist of a request by the owner and the approval by the board of supervisors or city council of the cancellation.

(2) A public hearing before the board or council.

(3) Notice of hearing by mail to each owner in the agricultural preserve of land under contract or agreement and publication of notice pursuant to section 6061 of the Government Code, provided, however, that a county or city may provide for such notice by ordinance instead of incorporating this requirement in the agreement.

(4) Findings by the board or council that cancellation is not inconsistent with the purposes of the Land Conservation Act of 1965 and is in the public interest.

The existence of an opportunity for another use of the land shall not be sufficient reason for cancellation. A potential alternative use of the land may be considered only if there is no proximate land not subject to a Land Conservation Act contract or agreement suitable for the use to which it is proposed the subject land be put. The uneconomic character of an existing agricultural use shall not be sufficient reason for cancellation. The uneconomic character of the existing use may be considered only if there is no other reasonable or comparable agricultural use to which the land may be put.

(d) Cancellation Fee-Waiver or Deferral. A provision for cancellation of the agreement must carry with it a cancellation fee payable by the owner to the county treasurer as deferred taxes which is at least 50 percent of the full market value of the land when relieved of the restriction, as found by the assessor, multiplied by the latest assessment ratio that had been published pursuant to section 251 of this code when the agreement was initially entered into. The determination of unrestricted value may be made the subject of an equalization hearing.

The agreement may provide for waiver or deferral by the board of supervisors or city council and may authorize the board or council to make the waiver or deferral contingent upon future action of the landowner if the agreement provides for a lien on the subject land securing the performance of the act upon which the waiver or deferral is made contingent. Waiver or deferral of the cancellation fee or a portion thereof may be allowed by the agreement if the waiver is subject to these findings by the board or council:

(1) It is in the public interest and the best interests of the program to conserve agricultural land that such payment be waived or deferred.